- Introduction

- Real World Assets explained

- How do RWAs work?

- Why do we need RWAs?

- RWA ecosystem

- RWA market players

- Key takeaways

Introduction

DeFi yields have fallen by over US$120B since November 2021, closely correlating with two-year lows in transaction volume and investor participation. To address this, Real World Assets (“RWAs”) are being tokenized and brought on-chain to be used as a source of yield within DeFi. RWAs can represent many different kinds of traditional assets such as commercial real estate, bonds, cars, and almost any other store of value that can be properly tokenized and accounted for. The most recent bear market has seen a significant period of development and growth within the RWA space, with TradFi institutions, such as Goldman Sachs, Hamilton Lane, Siemens, and KKR, working towards bringing their real world assets on-chain. This newsletter investigates the rapidly evolving RWA ecosystem and provides an in-depth market analysis and an overview of major players.

Real World Assets explained

Real World Assets (“RWAs”) are assets that exist off-chain, but are tokenized and brought on-chain to be used within DeFi. RWAs can represent tangible assets, such as gold and real estate, as well as intangible assets such as government bonds or carbon credits. The main driving force behind bringing real world assets onto the blockchain is the belief that DeFi will offer unique opportunities and market efficiencies to asset holders, which cannot be found in traditional financial systems.

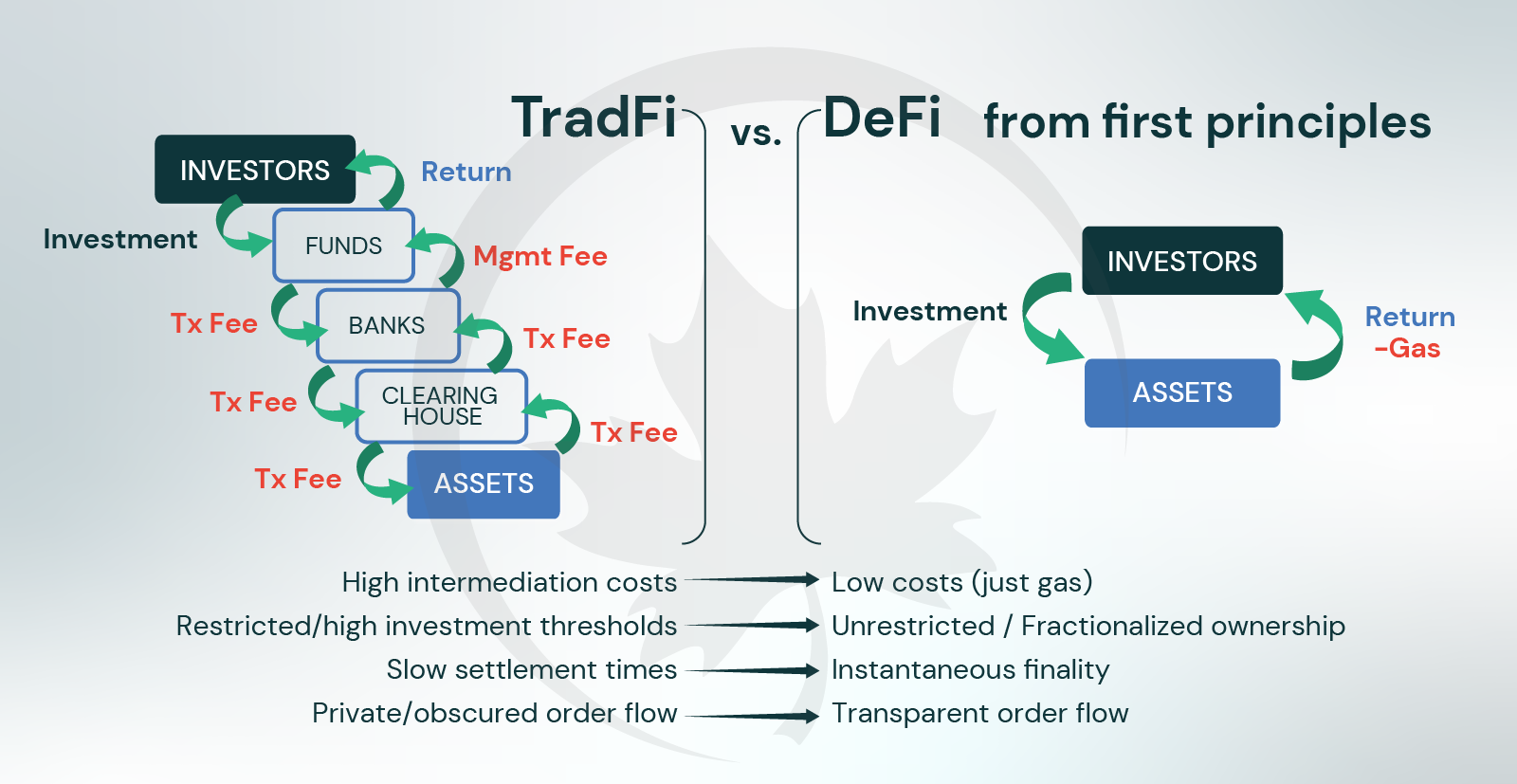

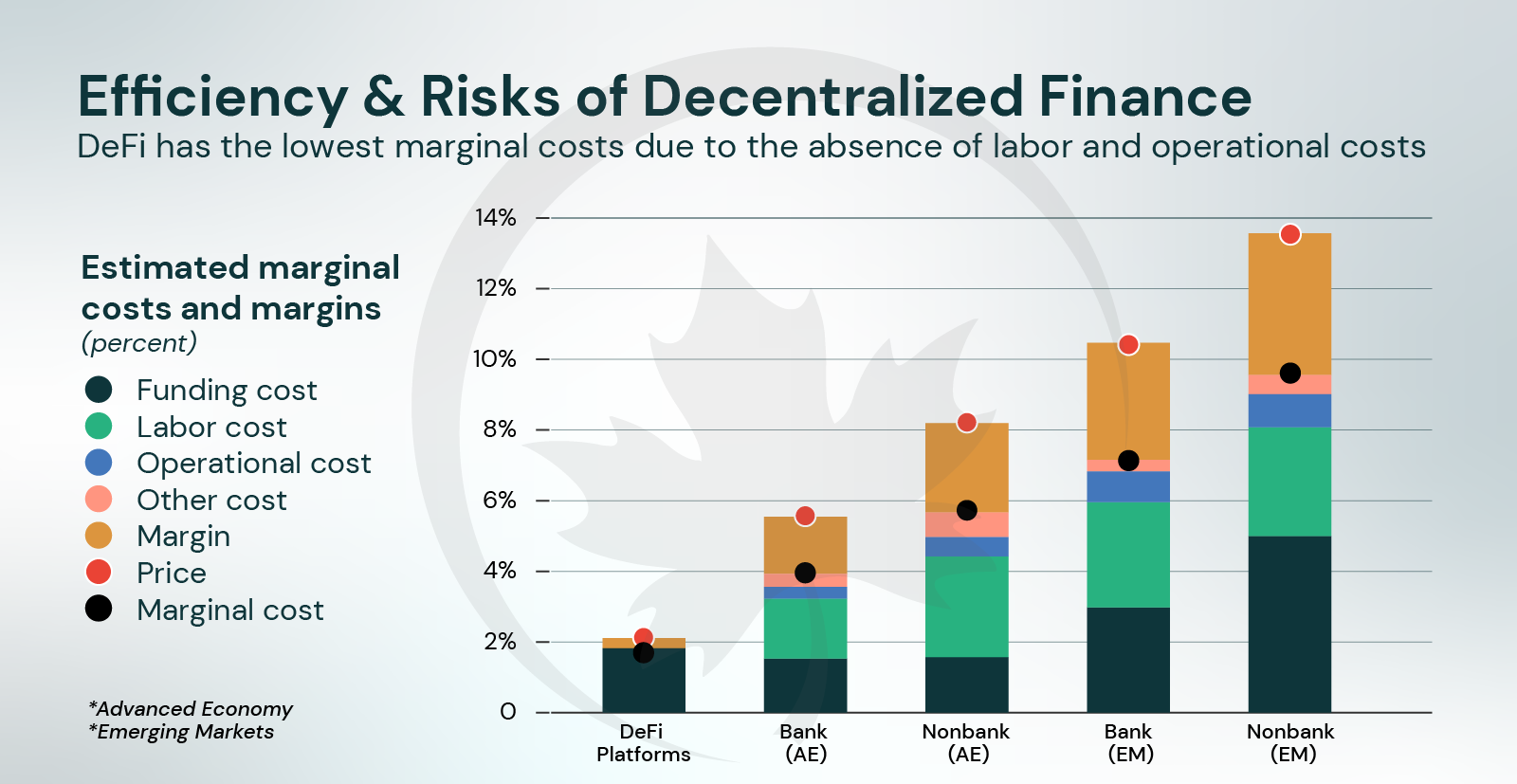

Decentralized financial systems (“DeFi”) have the potential to dismantle some of the constraints found within TradFi, and in turn, deliver material improvements in market efficiency and opportunities for asset holders. DeFi minimizes or completely cuts out the intermediation systems found in TradFi to effectively decentralize the back-end of financial markets. In the IMF’s 2022 Global Financial Stability Report, the IMF found that DeFi’s nuanced approach to financial markets results in outstanding cost savings as compared to TradFi systems. Additionally, idiosyncratic innovations found within DeFi such as Automatic Market Maker (“AMM”) models allow asset holders instantaneous access to liquidity and transaction finality, as well as the ability to easily fractionalize value and distribute exposure via digital tokens. Finally, the transparency of the blockchain ledger provides market participants with unique clarity into transaction flow, asset ownership, and mark-to-market prices. DeFi has the potential to prove as the superior back-end for financial systems, and asset holders may desire to represent their assets via RWAs in order to access improvements.

How do RWAs work?

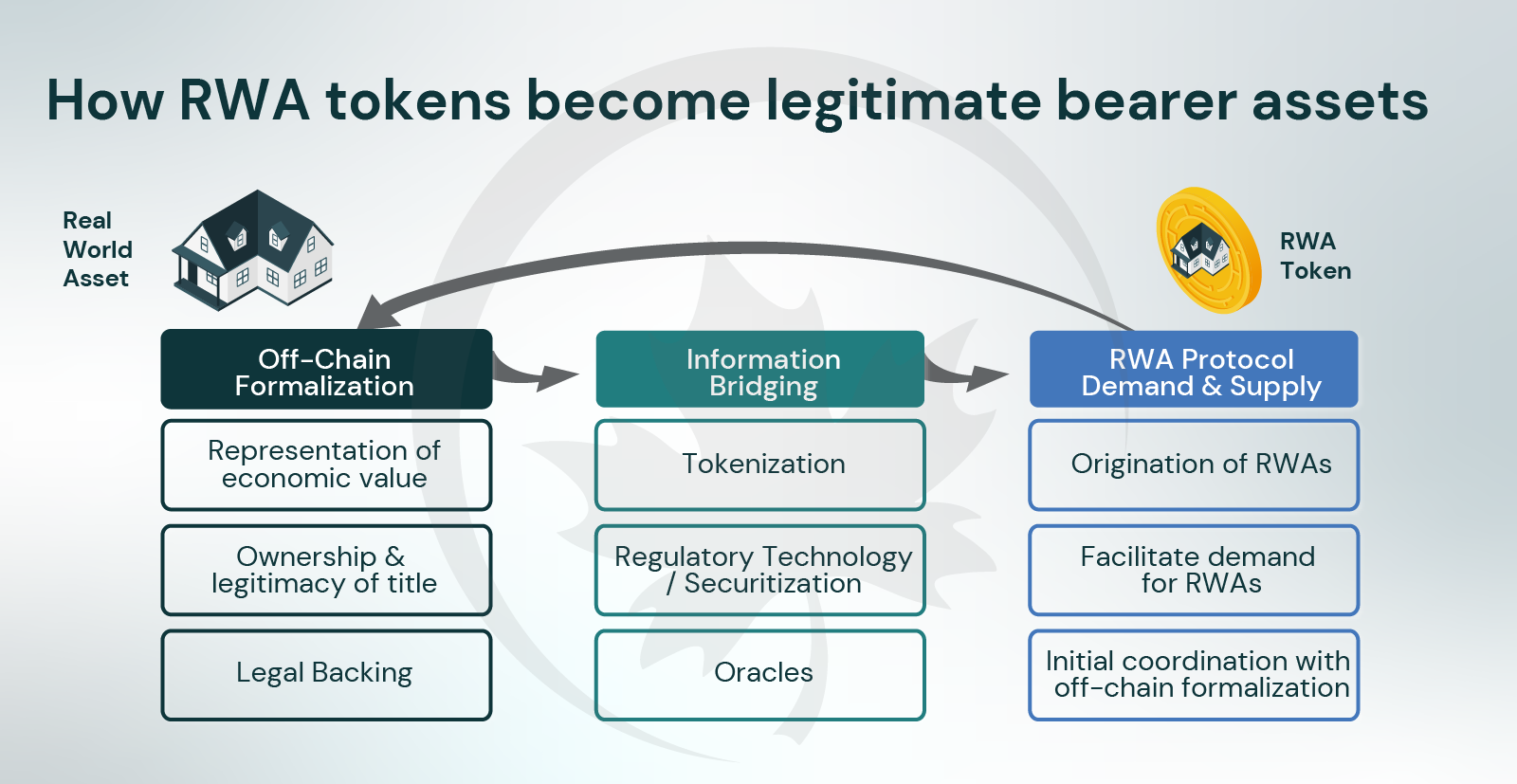

RWA tokens are tokenized representations of off-chain, real world assets. The process of RWA tokens becoming legitimate bearer assets can be conceptualized as three phases:

- Off-Chain Formalization

- Information Bridging

- RWA Protocol Demand and Supply.

Off-Chain formalization is necessary to ensure clarity in how much the asset is worth, who owns the asset, and which legal process protects any related property rights. Representation of economic value can be represented by the asset’s fair market value in traditional markets, its recent performance data, its physical condition, or other economic specifiers. Ownership & Legitimacy of Title can be formalized by a deed, a mortgage, an invoice, or any other reflection of one’s holdings. Legal backing should be provided for liquidations, dispute resolutions, and enforcement.

The next important steps in asset tokenization are: information bridging, regulatory technology/securitization, and RWA Protocol Demand and Supply. Information Bridging is the process of bringing on-chain information regarding an asset’s economic value and ownership to be stored within a blockchain ledger. Regulatory technologies include licensed security token issuers, crypto KYC/KYB providers, and cleared security token exchanges. Regulatory technologies are used to onboard assets into DeFi in a legally compliant way, while oracles are used to supply off-chain asset data to DeFi protocols. DeFi protocols serve as both the starting point of new RWA originations and the marketplace for RWA end products.

Why do we need RWAs?

The success of securitization in the 1990s is an example of how improved norms alter capital formation. It increased liquidity and originations, resulting in more affordable financing for consumers, companies, and house buyers. Securitization is virtually identical 30 years later, but financial markets have not yet evolved to accommodate the internet. The majority of assets cannot be securitized since they don’t fit neatly into a box during origination, and international financing markets are inaccessible to the majority of business owners. To cross TradFi’s moat, DeFi must build a link between crypto and the real world.

Despite the market for digital assets being small, the market for actual assets is enormous (>$600T). Crypto must address this sea of value if it is to have an impact on how business is conducted.

DeFi lending allows borrowers to access on-chain capital while using off-chain assets as collateral, providing up to 12% in annual savings to emerging market businesses. Blockchain’s efficiency allows network participants to enjoy near-instant loan settlements, and the adoption of RWAs within DeFi opens up the industry to the world’s largest debt markets. This approach will accelerate mainstream cryptocurrency adoption and provide a stepping stone for DeFi to reach its $100 trillion potential.

RWA ecosystem

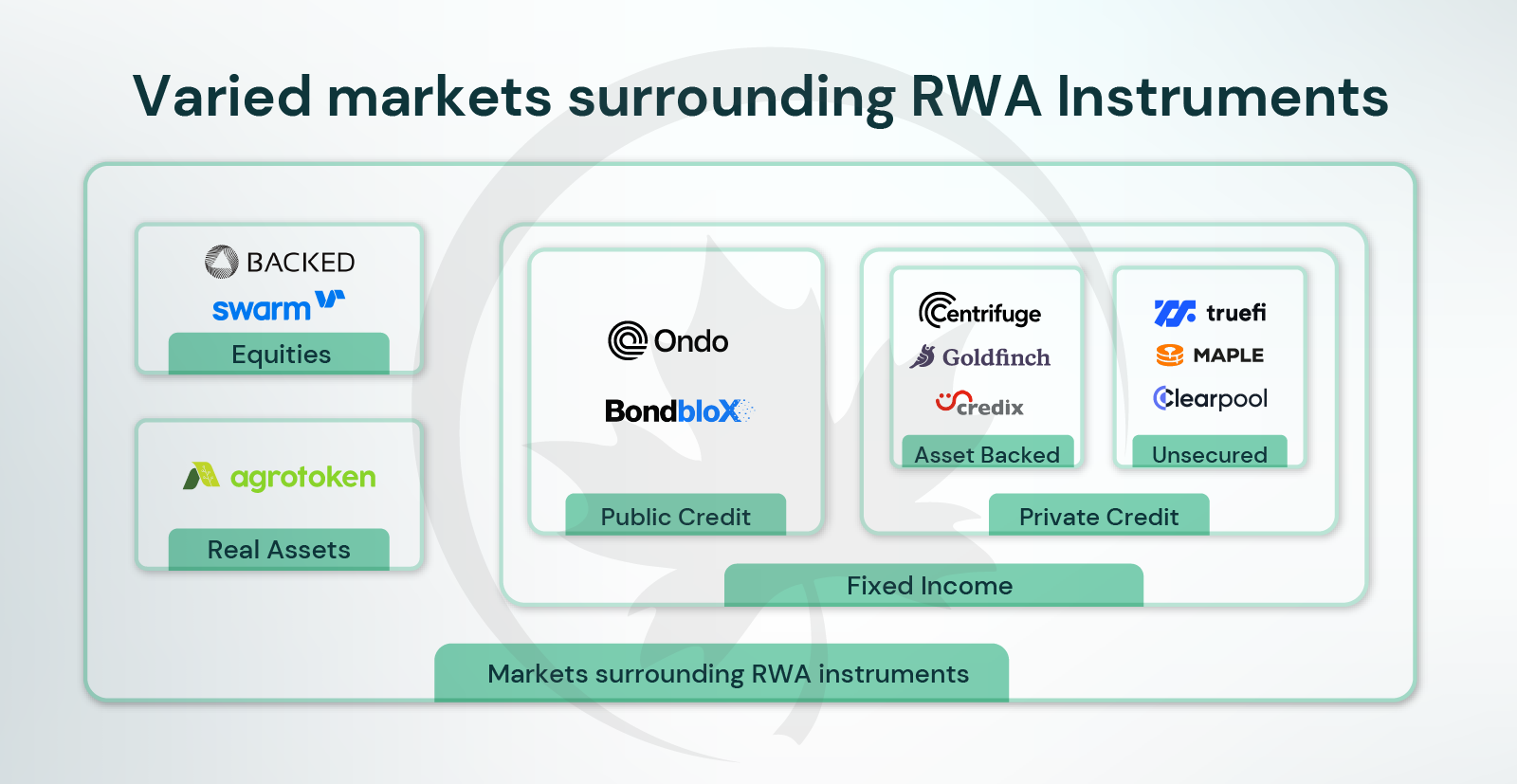

The RWA asset class has a diverse set of markets, with RWAs serving as the primary instrument for equity, real asset, and fixed income markets. Fixed income markets can further be segmented into private & public credit markets. Private credit based RWAs are abundant within DeFi, with over US$4B in total loan value across 1,560 different loans. The average interest rate on these loans is 9-9.75%. RWA private credit markets can further be segmented into two groups: asset-backed (or secured) private credit, or unsecured private credit (undercollateralized or not collateralized). Asset-backed private credit protocols orchestrate private credit markets in a way familiar to DeFi.

Crypto native lending/borrowing protocols, such as Maple, Clearpool, and TrueFi, allow businesses and institutions to borrow cryptocurrency while being undercollateralized with RWA assets or depositing no RWA collateral at all. These protocols have centralized background checks, due diligence procedures, and credit checks for borrowers and lenders.

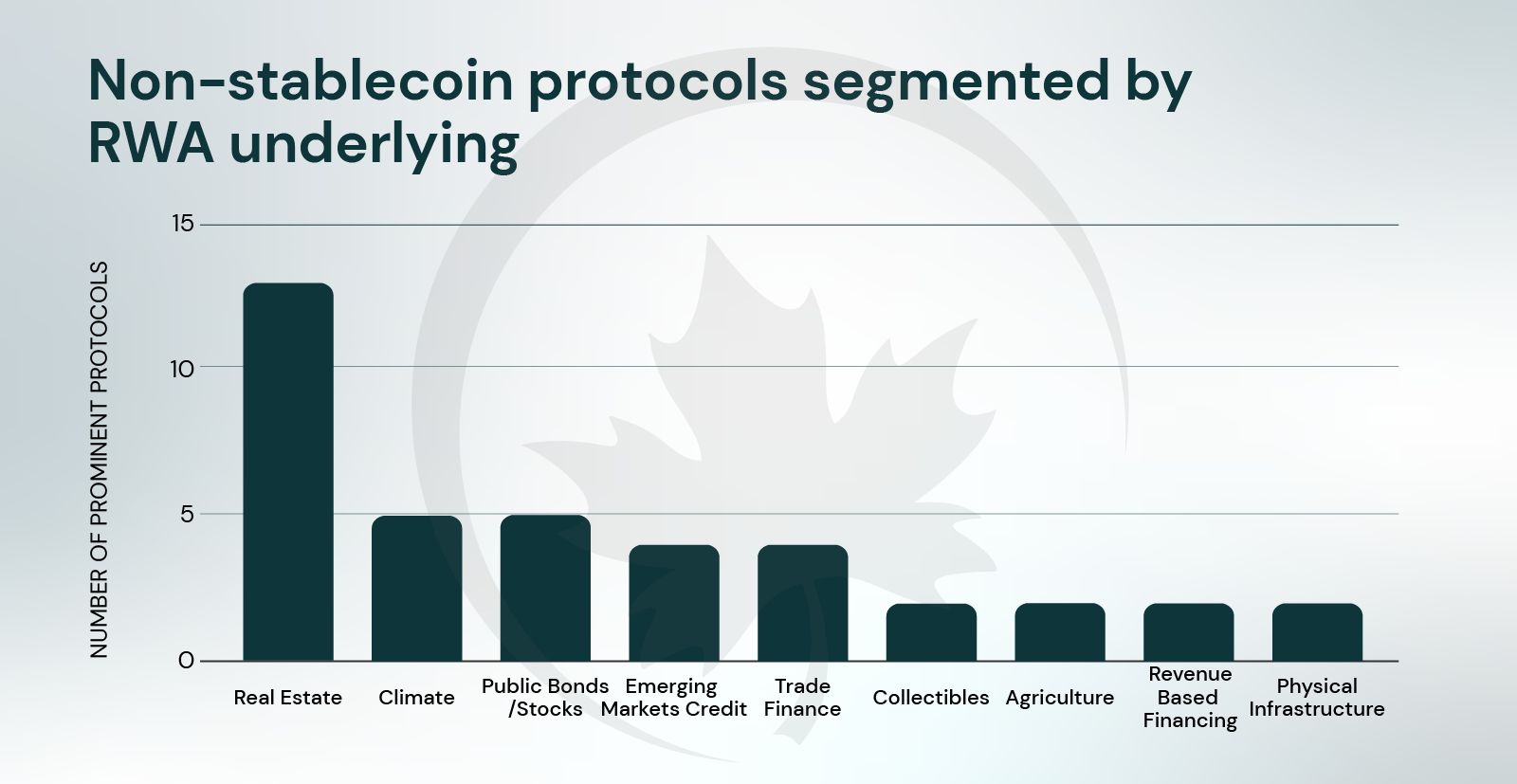

Stablecoins are the most popular underlying asset for RWAs, followed by real estate, climate-related underlyings, public bond/stock, emerging market credit, and so on.

RWA market players

MakerDAO

MakerDAO is a collateralized debt platform on Ethereum that allows borrowers to deposit collateral assets into “vaults” to take out debt denominated in the protocol’s native US$-based stablecoin, DAI. The types of collateral that can be used by borrowers is determined by the protocol’s governance DAO, MakerDAO, which voted to allow borrowers the ability to post RWA based collateral to vaults. The value of MakerDAO’s RWA vaults is over US$680M, allowing them to scale the amount of DAI issued into the market. MakerDAO has benefited from the interest revenue paid by RWA vault borrowers, generating an annualized US$23M of revenue. RWA vaults account for 56.7% of MakerDAO’s annualized revenue, and a number of different institutional borrowers have originated RWA collateralized vaults.

Goldfinch

Goldfinch is a protocol that allows businesses to access crypto lending without having to post crypto collateral. It has issued over US$120M of RWA based loans and has a unique way of vetting which businesses can become borrowers. It is developing a decentralized loan underwriting protocol that would enable anybody across the globe to issue loans on-chain using data like Unique Identity (UID) NFT, representing KYC/KYB. Goldfinch earns revenue through withdrawal fees and 10% of the interest payments as protocol reserves. The objective is to gather information created in both real life and online and use it to build a user’s reputation that can be applied on-chain. Protecting lenders involves preventing defaults and reimbursing lenders as much as possible.

Centrifuge

Centrifuge is a network that provides access to fast, cheap capital for small businesses and stable yield for investors. It uses a Proof-of-Stake consensus method to stake validators and offer adoption incentives. Tinlake, their first user-facing product, provides any firm to access DeFi liquidity with a simple method. Tranching allows investors to access different kinds of risk exposures and yields on the same asset class, and Centrifuge has created structures to allow investors access to tranches on a particular Tinlake debt offering. It also has an impressive network of crypto and TradFi partners, and recently announced a US$220M fund with MakerDAO and BlockTower Credit.

TrueFi

TrueFi is a leading credit protocol offering on-chain capital markets with a broad selection of real-world and crypto-native financial opportunities. It is owned and governed by holders of the TRU token, with underwriting owned by TrueFi DAO or independent portfolio managers. TrueFi has three layers of recourse in response to a default, including up to 10% of staked TRU slashed, a Secure Asset Fund for Users, and a Smart Contract Cover plan.

Maple

Maple is an uncollateralized borrow/lending protocol that hosts “pool delegates” to assess creditworthiness, set loan terms, and manage loan books. Maple LPs allocate capital to permissioned liquidity pools and receive back MPL interest. Maple is increasingly venturing into more RWA based loans, following last year’s centralized contagion that left Maple with US$52M in bad debt and up to 80% losses for select Maple LPs. In January, Maple created a US$100M liquidity pool backed by tax receivables.

Ondo Finance

Ondo Finance is bringing institutional grade products ranging from government bonds to high yield bonds to DeFi. They have created three investment funds, OUSG, OSTB, and OHYG, which tokenize them to become RWAs (called “fund tokens”). Users can trade fund tokens and use those fund tokens in permissioned DeFi protocols. Ondo Protocol is particularly noteworthy because it is one of the few protocols building out the public credit RWA market. This service has become highly demanded as a means of on-chain cash management, as real DeFi yields have decreased and interest rates have increased in the public credit markets.

Key Takeaways

- RWAs are becoming the bridge between TradFi and DeFi, catalyzing the development of the RWA ecosystem.

- Real World Assets (“RWAs”) are assets that exist off-chain but are tokenized and brought on-chain to be used as a source of yield within DeFi.

- For the first time, traditional assets such as bonds, real estate, carbon credits, etc. are being brought onto the blockchain, and DeFi native protocols and TradFi institutions will continue to build out the ecosystem.

- The main driving force behind bringing real world assets onto the blockchain is the belief that they will offer unique opportunities and market efficiencies to asset holders, which cannot be found in traditional financial systems.

- Fixed income is the predominant market in the RWA space, and there are a number of topical trends shaping the evolution of the RWA ecosystem like layer 1 RWA protocols, regulation and enforcement mechanisms.

- Blockchain is increasingly having real world use cases and proving its worth as a transformative technology.